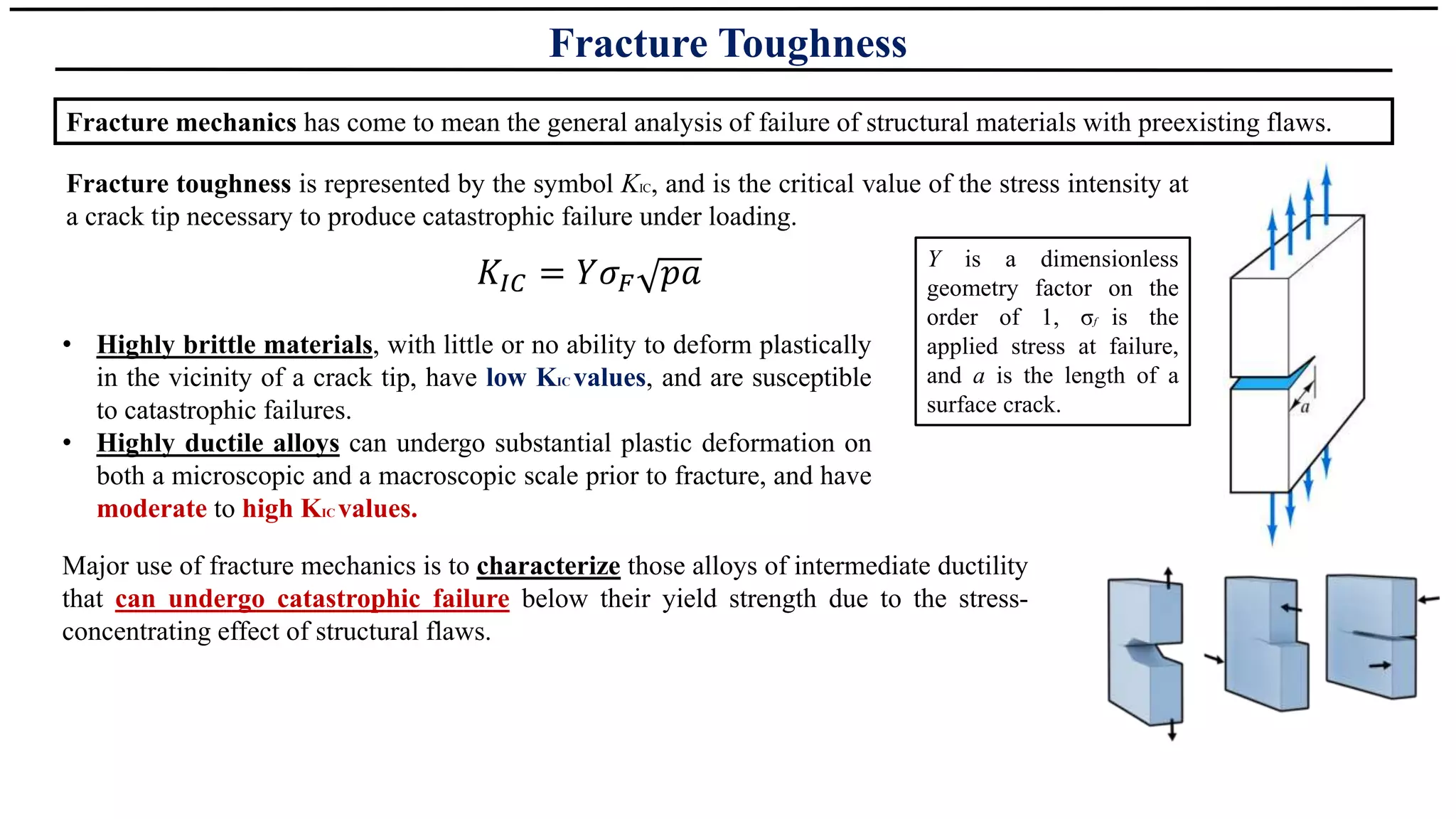

The image of a man hauling his deceased sister’s body into a bank in Odisha, India, represents more than a localized tragedy. It is the physical manifestation of a systemic collapse where rigid administrative protocols override basic human decency. On the surface, the incident involved a 70-year-old woman, Gunja Devi, and her brother, who felt forced to present her corpse to bank officials to release a measly sum of 1,500 rupees—money meant for her funeral rites. But the deeper investigative reality exposes a banking sector that has prioritized digital "Know Your Customer" (KYC) compliance over the very survival of its most vulnerable clients.

When the machinery of the state demands a thumbprint from a hand that no longer has a pulse, the system isn't just broken. It is predatory.

The Paperwork Trap and the Myth of Financial Inclusion

India has spent the last decade boasting about its financial inclusion revolution. Through the Jan Dhan Yojana scheme, millions of unbanked citizens finally received accounts, theoretically bridging the gap between the impoverished and the state’s welfare benefits. However, inclusion on paper does not equate to access in practice.

The core of the problem lies in the biometric authentication wall. In rural branches, managers are often terrified of audits. They operate under a culture of fear where any deviation from the rulebook—even for a pittance—can lead to professional ruin. This creates a scenario where "living proof" becomes the only acceptable currency. For Gunja Devi’s brother, the bank’s refusal to release funds without the account holder’s physical presence wasn't an isolated clerical error. It was the predictable outcome of a system that views account holders as data points rather than people.

Financial institutions have outsourced their common sense to algorithms and centralized databases. If the computer says the account holder must be present, the manager sees no alternative, even when faced with a grieving relative and a death certificate that hasn't yet cleared the slow-moving gears of local government offices.

The Disconnect Between New Delhi and the Village Square

The policy-makers in metropolitan hubs like New Delhi or Mumbai talk about "frictionless" banking. They envision a world of smartphones and high-speed data. Yet, the reality in districts like Ganjam or Nuapada is one of power outages, failed fingerprint scanners, and officials who treat the poor with a mixture of apathy and suspicion.

The Tyranny of the KYC Update

Banks are currently obsessed with KYC refreshes. This is ostensibly to prevent money laundering and fraud, but the impact on the elderly and the illiterate is devastating. To a high-level analyst, a KYC failure is a minor technical hurdle. To a woman living on less than two dollars a day, it is a gatekeeper that stands between her and her next meal, or in this case, her dignity in death.

We see a pattern here. This isn't the first time a body has been wheeled into a bank, and unless the underlying incentives change, it won't be the last. The "Business Correspondent" model, which was supposed to bring banking to the doorstep of the elderly, is frequently underfunded and poorly supervised. These middlemen often demand "service fees" that eat into the meager pensions of the poor, further alienating the very people the system was designed to help.

A Business Culture of Indifference

From a business perspective, the cost of serving the rural poor is high. The margins are thin, and the transactions are small. Consequently, banks often assign their least experienced or most disgruntled staff to these "punishment postings" in rural areas. The result is a toxic organizational culture where the customer is seen as a burden rather than a client.

When the bank manager in this case insisted on the physical presence of the deceased, he was acting as a cog in a machine that values process over purpose. The institutional failure is twofold:

- A lack of discretionary power: Branch managers have been stripped of the authority to make common-sense exceptions for fear of being flagged for "procedural lapses."

- Training deficits: Staff are trained to operate software, not to manage human crises. Empathy is not a metric tracked on a quarterly performance review.

The financial sector's obsession with "de-risking" has effectively turned the poor into a high-risk liability. By making it nearly impossible for a legitimate heir to claim a few thousand rupees, banks are protecting themselves against a theoretical fraud while committing a very real act of systemic cruelty.

The Fraud Fallacy

Bankers often defend these rigid stances by citing the risk of fraud. They argue that if they release money without strict verification, they open the door to relatives siphoning off pensions of the deceased. While fraud exists, the scale of "funeral fund" theft is microscopic compared to the multi-million dollar non-performing assets (NPAs) handed out to corporate moguls who flee the country.

The irony is sharp. A billionaire can default on a loan worth thousands of crores, yet a man in a tattered shirt is forced to drag a corpse across a marble floor to prove he isn't trying to steal twenty bucks. This disparity is why public trust in the institutional framework is evaporating.

The Cost of Digital Exclusion

Digital exclusion is the silent killer. When the state mandates that all benefits must flow through a bank account linked to a biometric ID (Aadhaar), it creates a single point of failure. If the scanner fails to read an elderly person's worn-down fingerprints, they are effectively erased from the system. They cannot buy food, they cannot get medicine, and, as we have seen, they cannot even die without the bank's permission.

This incident should be a wake-up call for the banking industry to implement a "Dignity Protocol." This would involve:

- Emergency Discretionary Funds: Allowing managers to release small sums for end-of-life expenses based on local verification.

- Mobile Verification Units: Ensuring that the bank goes to the customer when the customer is physically unable to travel.

- Simplified Survivorship Claims: Reducing the mountain of paperwork required for accounts with low balances (under 5,000 rupees).

The Path Forward is Not More Technology

The solution to a crisis of humanity is rarely more technology. Adding another layer of blockchain or a more "robust" AI verification tool won't help the man in the village. The answer lies in re-humanizing the frontline of finance.

Banks must empower their staff to be community liaisons rather than just data entry clerks. They need to understand that in the rural context, the bank is often the only link between a citizen and their basic rights. When that link becomes a barrier, the entire social contract begins to fray.

The Odisha incident is a stain on the record of modern banking. It serves as a reminder that "efficiency" is a dangerous goal when it ignores the messy, tragic, and undeniable reality of human life and death. The 1,500 rupees in Gunja Devi’s account was her money. The bank’s role was to be its custodian, not its jailer. Until the industry realizes that its primary duty is to the person and not the protocol, the sight of the dead being paraded through bank lobbies will remain a haunting possibility.

Banks must stop hiding behind the excuse of "compliance" to justify a lack of compassion. Compliance is a tool for order, but when it is used to deny the basic rights of the grieving, it becomes a weapon of the state. It is time to dismantle the paperwork wall and return to a banking model that recognizes the face of the customer—even if that face is no longer capable of providing a digital signature.

True financial inclusion requires a heart, not just a hard drive.