Capital allocation within Asia-Pacific markets currently faces a dual-axis compression. Investors are forced to price equity not based on localized earnings growth, but on the shifting delta of two geopolitical stressors: the structural reconfiguration of U.S.-China trade relations and the escalation of kinetic risk in the Strait of Hormuz. When regional markets open mixed, it is a mathematical reflection of localized bull sentiment being neutralized by systemic risk premiums. The current environment is defined by three specific friction points that dictate whether a portfolio maintains liquidity or suffers from sudden valuation haircuts.

The Geopolitical Risk Function

The "mixed" opening of Asian indices—specifically the Nikkei 225, Hang Seng, and ASX 200—is rarely a sign of indecision. It is the result of a calculated divergence in risk sensitivity. To understand why certain sectors rally while others retreat, one must apply a risk-weighting framework to the Trump-Xi summit and the Iranian maritime tensions. Meanwhile, you can read related stories here: The Battle for the Soul of Artificial Intelligence and the Musk Altman Schism.

The Trade Negotiation Matrix

The interaction between the U.S. and China is no longer a standard trade dispute; it has evolved into a competition over technological hegemony and supply chain sovereignty. Investors are tracking the Probability of De-escalation ($P_d$) against the Cost of Decoupling ($C_d$).

- Direct Tariff Impact: Traditional manufacturing sectors in Taiwan and Vietnam react to the immediate arithmetic of cost-plus pricing. If tariffs remain, the margin compression is a known variable.

- Technological Bipolarity: High-growth tech stocks in Shenzhen and Tokyo are pricing in a future where hardware and software stacks must be mutually exclusive. This creates a "dead zone" for companies that rely on both U.S. intellectual property and Chinese manufacturing scale.

- Currency as a Release Valve: The People’s Bank of China (PBOC) manages the yuan ($CNY$) as a strategic buffer. When trade tensions spike, $CNY$ depreciation acts as a subsidy for Chinese exporters but triggers capital flight from emerging markets, causing a sell-off in regional peripheral currencies.

The Energy Security Tax

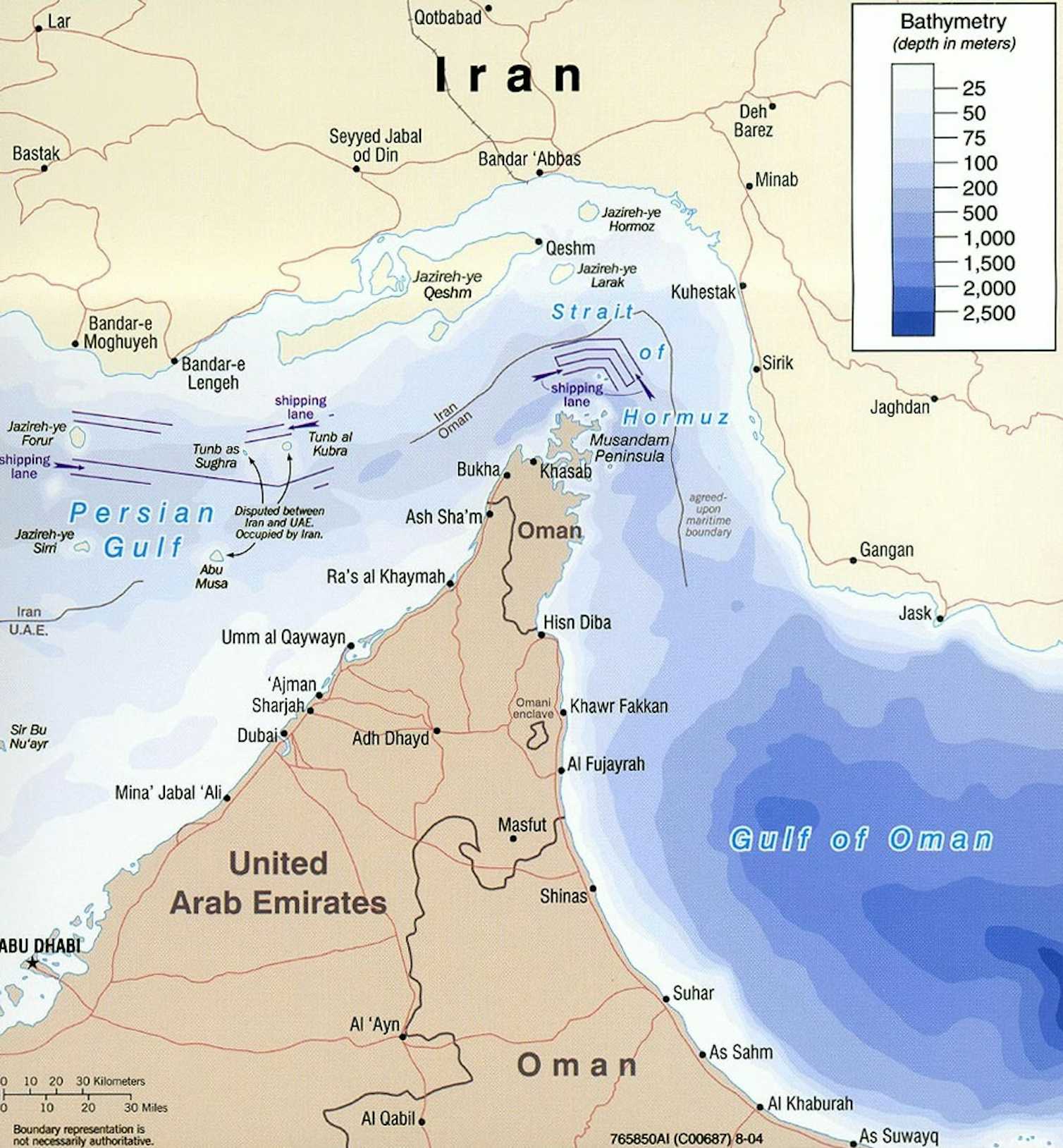

The Strait of Hormuz acts as a choke point for roughly 20% of the world's liquid petroleum. For energy-dependent economies like Japan and South Korea, Iran-related tensions represent an exogenous shock to the Input Cost Variable ($I_v$). To see the bigger picture, we recommend the recent report by The Economist.

- Freight and Insurance Premiums: As tensions rise, the cost of insuring tankers (War Risk Surcharges) increases. This cost is rarely absorbed by the shippers; it is passed down the value chain, manifesting as inflationary pressure in Seoul and Tokyo.

- The Strategic Petroleum Reserve (SPR) Lag: While nations have reserves, the psychological impact on the spot market creates immediate volatility. A $10 increase in the price of Brent crude functions as a regressive tax on Asian manufacturing, directly lowering the EBITDA projections for heavy industry.

Structural Divergence in Regional Indices

The "mixed" performance often cited in financial journalism hides a deeper structural truth: different Asian bourses are built on different economic engines, each reacting uniquely to global stressors.

The Export-Sensitive Model (Japan and South Korea)

The Nikkei and KOSPI are proxies for global consumer demand. When the U.S. and China—the world’s two largest consumers—are at odds, these indices face downward pressure regardless of internal fiscal health. The logic follows a simple path: Trade friction leads to reduced Capex (Capital Expenditure) in China, which reduces demand for Japanese precision machinery and Korean semiconductors.

The Financial and Property Hub (Hong Kong)

The Hang Seng Index is currently caught in a liquidity trap. It must balance the inflow of Chinese mainland capital with the outflow of international institutional funds fearing regulatory shifts. The risk here is not just trade; it is the Interbank Offered Rate (HIBOR) volatility. If the U.S. Federal Reserve maintains a hawkish stance to combat domestic inflation, the Hong Kong dollar’s peg forces a local rate hike, crushing property valuations and financial margins simultaneously.

The Defensive Resource Play (Australia)

The ASX 200 often moves inversely to its northern neighbors during times of tension. As a primary exporter of iron ore, LNG, and gold, Australia benefits from the "Flight to Quality." Gold prices typically appreciate during Iran-related instability, providing a floor for the ASX that manufacturing-heavy indices lack.

The Mechanics of Investor Hesitation

Vagueness in market sentiment is actually a period of Price Discovery under Extreme Uncertainty. Large-scale institutional investors (Pension Funds, Sovereign Wealth Funds) utilize a "wait-and-see" approach not because they are passive, but because the cost of being wrong on a geopolitical inflection point exceeds the opportunity cost of missing the first 2% of a rally.

The Information Gap in Diplomatic Summits

The Trump-Xi meeting is a high-variance event. There are three potential outcomes that analysts must model:

- The "Grand Bargain" (Low Probability): A comprehensive removal of tariffs and a framework for IP protection. This would trigger a massive short squeeze and a 5-10% rally across regional equities.

- The "Truce" (High Probability): A commitment to keep talking without further escalations. This maintains the status quo, leading to "mixed" openings as markets price in prolonged uncertainty.

- The "Breakdown" (Medium Probability): New tariffs and a cessation of talks. This leads to a systematic re-rating of Asian growth, forcing a rotation into defensive utilities and sovereign bonds.

Quantitative Easing and Central Bank Limits

Asia’s ability to "spend its way out" of these tensions is reaching a ceiling. With high debt-to-GDP ratios in several ASEAN nations, the ability to deploy further stimulus is constrained. Investors are monitoring the Spread between Policy Rates and Inflation ($R-i$). If inflation driven by energy costs rises faster than central banks can adjust, real returns turn negative, making equity markets fundamentally unattractive.

The Strategic Playbook for Volatile Openings

In a market defined by the intersection of trade wars and kinetic conflict, the standard "buy the dip" mentality is insufficient. Strategic capital preservation requires a transition toward Relative Value (RV) Trading.

- De-risk the Technology Sector: Until a clear regulatory framework emerges from the U.S.-China summit, technology weightings should be shifted toward companies with diversified supply chains (e.g., those moving operations to India or Mexico).

- Long Energy/Short Manufacturing: This pair trade hedges against Iran-related spikes. The gain in energy holdings offsets the increased input costs in the manufacturing portfolio.

- Currency Hedging: Institutional players must utilize $USD/JPY$ or $USD/CNH$ forwards to protect against the "Safe Haven" surge. In times of crisis, the Yen often strengthens despite Japan's proximity to the conflict, creating a paradox that can wipe out equity gains for foreign investors.

The current "mixed" state of Asia-Pacific markets is the equilibrium point of a high-stakes geopolitical equation. The variable that will break this equilibrium is not a domestic economic report, but the tone of a single press conference or a single incident in the Persian Gulf. Investors must prioritize liquidity over alpha until the structural friction between the world's two largest economies shows a measurable decrease in tension.