The headline number is 3.3 percent. It is the kind of figure that invites quick analysis, a collective sigh of relief that the sky has not fallen, and a return to business as usual. But anyone who has spent decades watching the machinery of the British economy knows that headline rates are often a distraction. They are the shiny object meant to pull attention away from the structural decay occurring beneath the surface.

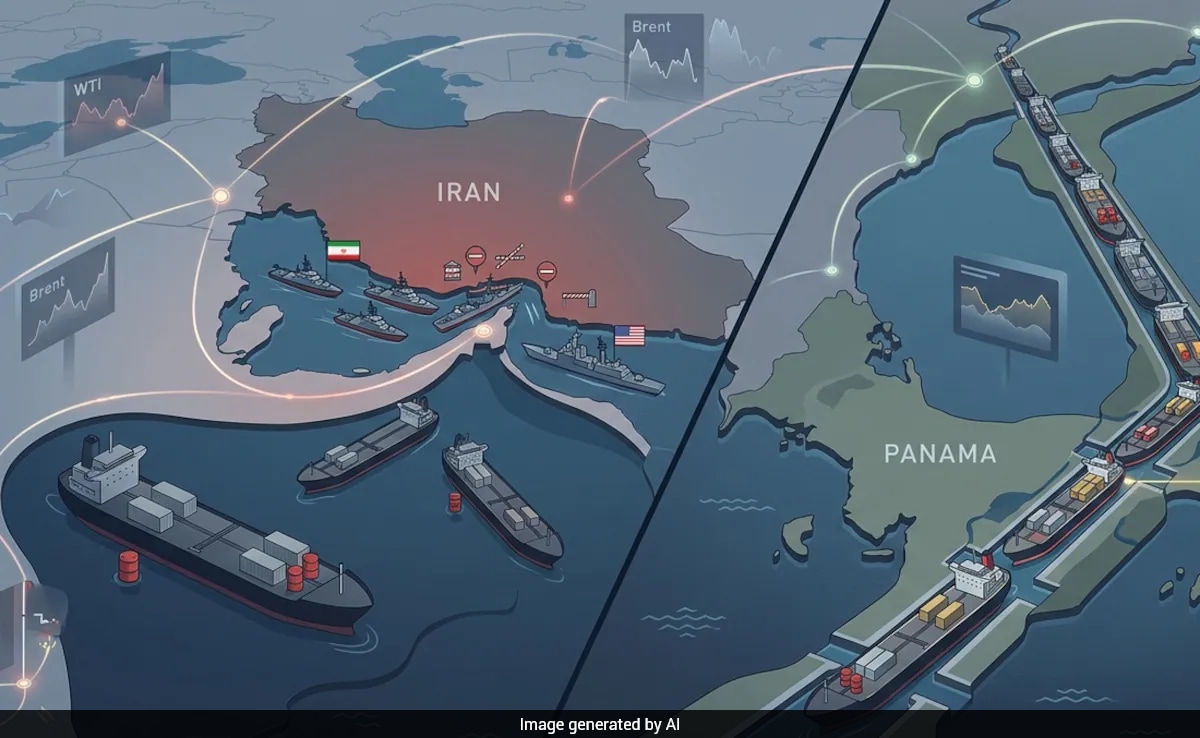

This latest rise in inflation, driven heavily by an 8.7 percent jump in motor fuel prices, is not merely a statistical anomaly linked to geopolitical volatility in the Middle East. It is a symptom of a much deeper, more systemic vulnerability that the United Kingdom has spent years failing to address. The disruption in global energy markets—triggered by the conflict involving Iran and Israel—is simply the catalyst. It has exposed the brittle nature of a supply chain that assumes stability in regions where stability is a luxury, not a given.

Fuel prices are the most visible element of this inflation, acting as a tax on every movement of goods and people. When petrol and diesel costs rise, the shockwaves travel through every corner of the economy. The cost of transporting food from farm to supermarket, the expense of delivery services, and the overheads for manufacturing firms all swell in lockstep. This is the multiplier effect. It ensures that while the fuel price hike appears to be the primary actor, it is actually the conductor of a much broader, more persistent inflationary orchestra.

To understand why this is happening now, look at the composition of the current inflationary environment. While the overall Consumer Prices Index reached 3.3 percent in March, the real concern for policymakers is not the fuel component. It is the services sector. Services inflation, which climbed to 4.5 percent, suggests that price increases are becoming embedded in the domestic economy. This is where the danger lies. When companies begin to raise prices in response to energy costs, and workers demand higher wages to maintain their living standards in response to those prices, the economy enters a self-reinforcing cycle.

The Bank of England faces a dilemma that standard economic textbooks struggle to solve. On one hand, raising interest rates to suppress inflation risks suffocating an economy that is already fragile. On the other hand, allowing inflation to remain elevated risks devaluing the currency further and ensuring that the cost of living remains a permanent burden for millions of households. They are trying to extinguish a fire with a leaking hose, constantly balancing the need for price stability against the fear of a deep, prolonged recession.

Consider the role of food inflation, which sits at 3.7 percent and is poised to accelerate. The closure of shipping routes and the threat to global fertiliser supplies means that the food on the shelves is not just getting more expensive due to transport costs; it is becoming a scarce commodity. There is a lag in how these costs hit the consumer. What we see at the checkout today is only the beginning. Industry bodies have already issued warnings that this figure could climb significantly higher before the year is out. If that happens, the 3.3 percent inflation figure will look like a historical footnote in a much grimmer narrative.

There is also the matter of the exchange rate. The pound remains vulnerable to sentiment shifts. Every time a new headline emerges about the conflict or the resulting energy supply constraints, investors react by tempering their expectations for the UK economy. This creates a feedback loop. A weaker pound makes imports more expensive, which drives domestic inflation higher, which in turn weakens the currency further. It is a cycle of depreciation that creates a permanent, albeit fluctuating, inflationary headwind.

Industry analysts often talk about supply chain diversification, but in practice, the UK remains tethered to a handful of global energy sources. The reliance on imported energy is not just a policy choice; it is a geographic and historical reality that requires a monumental shift to alter. That shift is not happening at the pace required. While renewable energy targets are ambitious, the current energy mix remains heavily tied to fossil fuel prices that are set in global markets, not by domestic policy.

This vulnerability is particularly acute for manufacturers. A factory that relies on energy-intensive processes cannot simply absorb an 8.7 percent jump in fuel costs without passing that burden along. They have three options. They can absorb the costs and accept lower margins, which eventually leads to job cuts or capital flight. They can increase prices, which adds to the headline inflation rate. Or they can cease operations altogether. In a competitive global market, the latter is increasingly becoming a rational response.

The workforce is not immune to these pressures either. Real wages have struggled to grow in meaningful terms for years. When inflation eats into purchasing power, the inevitable response is labor unrest or, more commonly, a quiet exodus of talent. When skilled workers see their disposable income vanish, they seek better opportunities. This leads to a tight labor market in certain sectors, which in turn forces employers to raise wages to attract and retain staff. Those wage increases are then passed on to consumers, fueling more inflation. This is the wage-price spiral that central bankers lose sleep over.

The geopolitical dimension is equally important. The current state of affairs in the Middle East is not just a short-term crisis. It is a long-term alteration of the global trading map. The Strait of Hormuz is a narrow bottleneck that the entire global economy relies upon. When that bottleneck is restricted, the cost of global trade rises. It is as simple as that. Pretending that the UK can insulate itself from these global forces is an exercise in futility. The UK is a trading nation, and it is inextricably linked to the price of oil and gas regardless of its own domestic output.

We must also examine the behavior of retail giants. There is a persistent belief that when wholesale prices rise, retail prices follow immediately. But that is rarely the case. Retailers often utilize a "rocket and feather" pricing strategy. Prices rise like a rocket when wholesale costs increase, but they fall like a feather when those costs stabilize. This is not necessarily malice; it is risk management. Retailers are hedging against future volatility. However, the result for the consumer is the same: prices remain high long after the initial cause of the spike has abated.

Furthermore, the government's role in this current inflationary environment is constrained by its own debt levels. There is limited fiscal space to provide support to consumers without further stoking the flames of inflation. The Chancellor is walking a tightrope. Every pound of support offered to households is another pound that must be borrowed or taxed, both of which have their own inflationary consequences. There is no easy path through this situation.

What then is the realistic outlook for the remainder of the year? Most analysts expect inflation to fluctuate between 3 percent and 4 percent. This is not the catastrophe some might have predicted, but it is certainly not the 2 percent target that is the bedrock of economic policy. It is a sticky, persistent form of inflation that erodes wealth without triggering the kind of drastic intervention that a higher rate might demand. It is a slow, grinding decline in standard of living.

This is the reality of the current economic environment. We are not dealing with a temporary shock that will resolve itself in a few months. We are dealing with a structural realignment of the economy. Energy is more expensive, labor is more expensive, and supply chains are less efficient than they were five years ago. These are the ingredients for a period of sustained inflation that will persist even if the immediate geopolitical tensions in the Middle East begin to ease.

When looking at the figures, it is easy to become fixated on the cause of the latest jump. But the cause is secondary to the consequence. The consequence is that the UK economy is becoming less capable of absorbing shocks. Each successive crisis, whether it is energy prices, supply chain disruptions, or labor market tightness, leaves the economy a little more weakened.

The question for investors, policymakers, and ordinary citizens is not when inflation will return to 2 percent. The question is how to build an economy that can function effectively in a world where 3 percent or 4 percent inflation is the new normal. That requires a fundamental rethink of everything from energy policy to labor market regulations and tax incentives. It requires acknowledging that the old models of economic management are no longer fit for purpose.

For the individual, the takeaway is clear. Do not expect relief from macro-level policy shifts. The inflation of the last few years has changed the math of personal finance. Savings that were adequate a decade ago are no longer sufficient. Strategies that worked in an environment of low, stable inflation are now liabilities. The era of cheap money and predictable price movements is over, and it is not returning in the foreseeable future.

Ultimately, the 3.3 percent headline figure is a warning. It is a signal that the economic engine is running hot, not because of a temporary acceleration, but because of friction in the components. Ignoring the signs will only ensure that the next spike in prices—whether from another energy disruption or a supply chain failure—hits an economy that is even less prepared to handle the impact. The time to adjust is now, before the heat becomes a fire that the current tools of statecraft are unable to extinguish.